With mature, cyclical sectors set to rebound as the economy returns to some semblance of normal, High Yield gets ready for its Goldilocks moment.

For more of Bruce’s insights, watch our High Yield Update videos.

By Bruce H. Monrad, Chairman, Northeast Investors Trust | January 2021

Click here to read a PDF of this article.

In 2020, soon after the initial shocks from the Covid recession wore off, we started to sense a potential ‘Goldilocks’ scenario forming in High Yield.

In the late spring and summer, the Federal Reserve began taking unprecedented steps to support the credit markets, assuring investors that interest rates would stay near zero through at least 2022. That was followed in the fall by signs of a reasonably strong rebound, as businesses shuttered by social distancing restrictions began to reopen. Then came fiscal stimulus from Washington, along with indications from the incoming Biden administration that more relief could be on the way in 2021.

Finally, in December, the economy got a real shot in the arm (pun intended) with the rollout of the first Covid vaccines, offering hope that the economy could return to some sense of normalcy in 2021. As that recovery broadens out into ‘old economy’ parts of the market in the coming year, we expect Goldilocks to come into even sharper focus for High Yield.

The Positive Real Economy

Even before the first batches of the Pfizer-BioNTech and Moderna vaccines rolled out in late December, the economy was starting to emerge from the recession that began at the start of the pandemic in February 2020. Signs of strength could be seen in housing, manufacturing, and shipping. In fact, the Cass Freight Index, a barometer of North American shipping activity, climbed above its pre-pandemic levels in the fall and is now signaling greater activity than at the start of the last expansion, in June 2009.

More importantly, momentum has started to show up in key cyclical sectors. In the fourth quarter, energy, industrials, and consumer discretionary companies experienced the biggest earnings decline in the S&P 500. Yet in 2021, those sectors—which represent three of the five biggest weightings in High Yield— are expected to see the largest corporate profit gains, according to FactSet.

At the same time, pandemic plays that thrived in 2020 such as tech, healthcare, and consumer staples—and that aren’t reliant on a sizzling economy—are all expected to see slower-than-average growth in 2021.

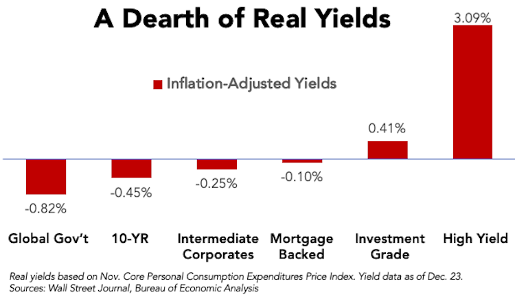

Negative Real Yields

Heading into the new year, High Yield enjoys a big competitive advantage: The dearth of yields anywhere else in fixed income. Amazingly, fewer than 15% of all global bonds sport yields above 2%, according to Deutsche Bank. At the same time, an unprecedented array of bonds are sporting negative nominal yields or negative real yields, after accounting for inflation.

On sovereign debt alone, there’s now $31 trillion in bonds with negative real yields. In the U.S., real yields throughout the entire Treasury curve—including on 30-year bonds—are less than zero. As for investment-grade corporates, the real yield on the Bloomberg Barclays investment-grade corporate bond index has fallen to 0.4%. That means unless you’re willing to go out at least 10 years or longer in maturity, exposing yourself to greater duration risk, the income thrown off by investment-grade bonds today is being swamped by inflation.

By contrast, High Yield bonds are paying out around 4.5%. With core personal consumption expenditures rising at a 1.4% annual clip in November, that’s a real yield of more than 3%.

Conclusion

Think about the underlying conditions needed for High Yield to outperform. Many of those factors are in place now.

For starters, assets that compete for capital with High Yield are now at a competitive disadvantage—Treasuries owing to their negative real yields and stocks due to historically high valuations. We’re in the early stages of a recovery, which is when risk assets like High Yield tend to outperform. Cyclicals, representing a big chunk of High Yield issuers, are gaining traction. What’s more, the economy is neither too cold (so credit risk is under control) nor too hot (so rates remain low, encouraging investors to look for higher yields).

It is possible that we could start seeing a little bit of inflation in 2021. For High Yield, however, the presence of modest amounts of inflation could turn out to be just right—just enough to benefit old economy issuers with real assets on their books and just enough for investors yearning for income to focus on real yields.

Bruce H. Monrad is chairman and portfolio manager of Northeast Investors Trust (ticker: NTHEX), a no-load, high-yield fixed income fund, whose primary objective is the production of income. Bruce is among the longest-tenured bond fund managers, having run Northeast Investors Trust for more than 30 years. He received his A.B. from Harvard College and his M.B.A. from Harvard Business School.

CONTACT: 1-800-225-6704 (M-F 9:00am – 4:45pm EDT); bmonrad@northeastinvestors.com

Join our email list to get the latest informed news and commentary from Northeast Investors Trust.

Click here to read a PDF of this article.

DISCLAIMER: From time to time a Trustee or an employee of Northeast Investors Trust may express views regarding a particular company, security, industry or market sector. The views expressed by any such person are the views of only that individual as of the time expressed and do not necessarily represent the views of the Trust or any other person in the Northeast Investors Trust organization. Any such views are subject to change at any time based upon market or other conditions, and Northeast Investors Trust disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for Northeast Investors Trust are based on numerous factors, may not be relied on as an indication of trading intent on behalf of the Trust.